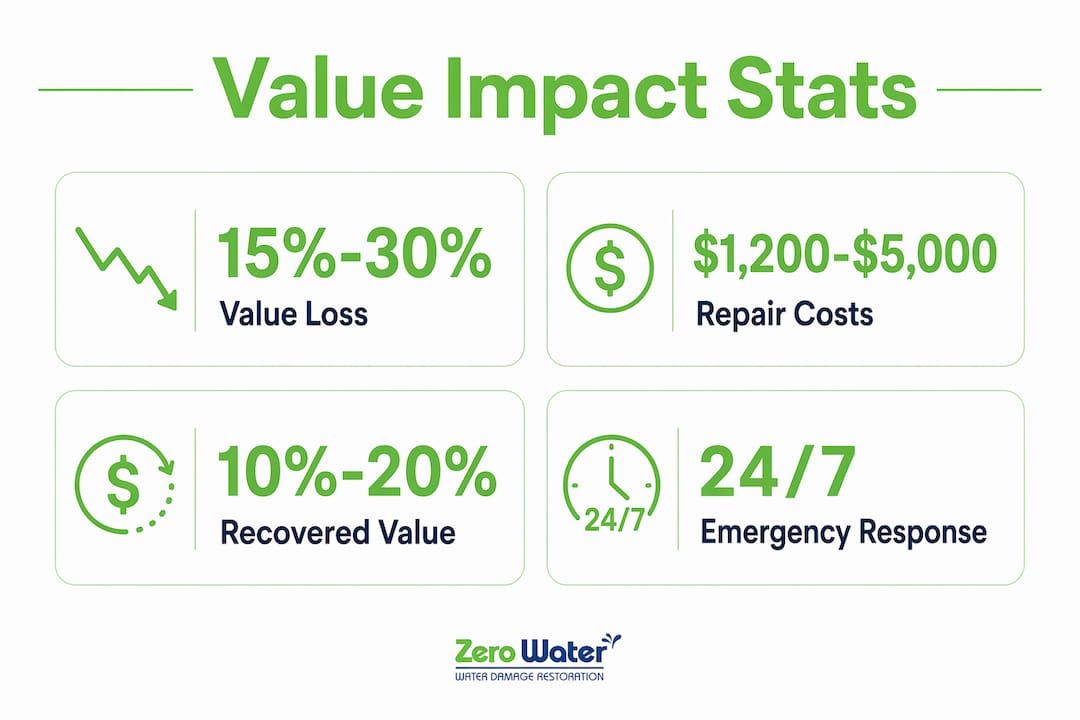

Water damage reduces a home’s market value by 10% to 30%, and in severe untreated cases, properties can sell for as little as 50% to 70% of their after-repair value. The financial hit goes beyond visible stains and warped floors. It reaches into appraisal reports, mortgage approvals, and buyer psychology in ways most homeowners don’t anticipate until they’re already in the middle of a sale. Understanding how water damage affects home value, and what you can do about it, is the difference between recovering your equity and leaving serious money on the table.

How water damage affects home value: the core factors

Homes with past water damage typically sell for 15% to 30% less than comparable undamaged properties. That range isn’t arbitrary. It reflects a combination of structural risk, health concerns, financing obstacles, and the psychological weight buyers assign to a property with a troubled history.

Several specific factors drive that value loss:

- Structural compromise. Water weakens wood framing, subfloors, and load-bearing elements over time. Buyers and appraisers treat structural uncertainty as a major liability, not a cosmetic issue.

- Mold growth. Mold can colonize within 24 to 48 hours after water intrusion. Once present, it triggers health concerns, requires professional remediation, and creates legal exposure for sellers who fail to disclose it.

- Visible deterioration. Stained ceilings, buckled hardwood, and peeling paint signal neglect to buyers. Even after repairs, cosmetic evidence of past damage can suppress offers.

- Financing barriers. Lenders routinely decline or delay mortgage approvals when active leaks, mold, or unresolved structural issues are present. A home that can’t be financed conventionally loses a significant portion of its buyer pool.

- Appraiser deductions. Appraisers subtract estimated repair costs and apply a stigma discount of up to 20% when valuing a water-damaged property. That double deduction compounds the financial impact.

Pro Tip: Document every repair with photos, receipts, and contractor reports. Appraisers require clear evidence of remediation, and a well-documented repair history can meaningfully reduce the stigma discount applied to your home’s value.

The unknown risks of water damage extend beyond what’s visible. Moisture trapped inside walls or under flooring can compromise structural integrity for months before any outward sign appears, which is exactly why buyers and their inspectors treat water history with such caution.

How do appraisals, inspections, and lender requirements affect selling?

Financing is where water damage most directly controls your sale outcome. Mortgage lenders require that properties with disaster-related damage affecting safety or structural integrity be repaired before loan delivery. Minor cosmetic damage may allow closing if repair funds are escrowed, but active problems stop approvals outright.

Here is how the process typically unfolds when a water-damaged home enters the market:

- Home inspection. The buyer’s inspector identifies current or past water damage, documents affected systems, and flags unresolved issues. Any active moisture or mold triggers immediate concern.

- Appraisal. The appraiser reviews inspection findings, requires documented photos of all damage and repairs, and assigns value based on current condition. Incomplete documentation leads to “subject to” conditions that delay or kill the sale.

- Lender review. Underwriters apply Fannie Mae and Freddie Mac guidelines to determine whether the property meets minimum condition standards. Properties that fail on safety, structural soundness, or core system functionality are ineligible for conventional financing until repairs are complete.

- FEMA-style safety criteria. Even outside formal disaster zones, FEMA inspectors evaluate electrical, gas, plumbing, and structural systems to determine habitability. These same criteria inform how appraisers and lenders assess market readiness.

- Disclosure requirements. Sellers are legally required to disclose known water damage history in most states. Undisclosed damage discovered after closing creates liability and can unwind a completed sale.

“Resale and financing impact often rely more on the home’s current safety, structural soundness, and system functionality than on visible stains.” The implication is clear: a home that looks fine but has unresolved system damage will still fail lender scrutiny.

Lender guidelines effectively treat structural and health-related water damage as mandatory repair items. This isn’t a negotiating point. It’s a hard stop in the underwriting process that removes conventional buyers from your pool until the issues are resolved.

What are the costs and benefits of repairing water damage before selling?

The repair-versus-sell-as-is decision is the most consequential financial choice a homeowner with water damage faces. The math is not always straightforward, but the data provides a clear framework.

Minor water damage repairs typically cost between $1,200 and $5,000, covering issues like drywall replacement, minor flooring repairs, and basic mold treatment. Major structural repairs, including foundation work, framing replacement, or extensive mold remediation, range from $15,000 to $70,000 or more. Repaired homes generally sell for 10% to 20% more than unrepaired counterparts, but stigma can still reduce the final price even after full remediation.

| Scenario | Typical cost | Expected sale outcome |

|---|---|---|

| Minor repairs completed | $1,200 to $5,000 | Eligible for conventional financing; broader buyer pool |

| Major repairs completed | $15,000 to $70,000+ | 10% to 20% value recovery; stigma discount may remain |

| Selling as-is to investors | $0 upfront | 50% to 70% of after-repair value; fast close, no repairs |

| Undisclosed damage discovered | Variable | Legal liability, sale reversal, or price renegotiation |

Selling as-is attracts cash buyers and real estate investors who price in the repair costs and a risk premium. You close faster and avoid the repair process entirely, but you absorb the largest financial loss. For homeowners with limited capital or time, that tradeoff can make sense. For those with equity to protect, completing at least the structural and mold-related repairs before listing almost always produces a better net outcome.

Pro Tip: Get a pre-listing inspection before deciding whether to repair or sell as-is. Knowing exactly what a buyer’s inspector will find lets you price accurately, repair strategically, and avoid last-minute renegotiations that cost more than the repairs would have.

Making temporary repairs for water-damaged homes quickly after an incident can also stabilize the property and prevent secondary damage from escalating repair costs before you make the longer-term decision.

How can homeowners prevent or limit the impact on property value?

Prevention and rapid response are the two most effective tools for protecting your home’s value after water intrusion. The window between an incident and lasting damage is narrow.

- Act within 24 to 48 hours. Prompt extraction and drying within this window is critical to preventing mold colonization and structural decay. Every hour beyond that threshold increases remediation costs and the probability of permanent damage.

- Maintain your roof, gutters, and plumbing. Most residential water damage originates from preventable sources: clogged gutters that overflow into foundations, aging supply lines that fail, and roof flashing that separates over time. Annual inspections of these systems cost far less than a single water event.

- Invest in professional mold remediation when needed. DIY mold treatment addresses surface growth but rarely eliminates the source. Professional remediation, including moisture mapping and containment, is what appraisers and buyers expect to see documented.

- Keep detailed records of all maintenance and repairs. A binder with contractor invoices, inspection reports, and before-and-after photos is one of the most underrated tools for protecting resale value. It gives appraisers the evidence they need to minimize stigma deductions.

- Understand your insurance coverage before you need it. Standard homeowners policies typically cover sudden and accidental water damage but exclude flooding and gradual leaks. Knowing your coverage limits before an event determines how quickly you can fund repairs and protect your equity.

Pro Tip: After any water event, contact your insurer before starting major repairs. Premature demolition or material removal can void coverage. Document everything with photos and video first, then begin extraction and drying.

Protecting your home against water damage starts with understanding where your property is most vulnerable. A professional assessment after any moisture event gives you a clear picture of what needs immediate attention versus what can be monitored over time.

Key takeaways

Water damage lowers home value through a combination of structural risk, mold exposure, financing barriers, and appraiser stigma discounts that compound each other and are difficult to reverse without professional remediation.

| Point | Details |

|---|---|

| Value loss is significant | Homes with water damage history sell for 15% to 30% less, or as low as 50% to 70% of after-repair value when sold as-is. |

| Lenders enforce hard stops | Structural or safety-related water damage must be repaired before conventional mortgage approval under Fannie Mae and Freddie Mac guidelines. |

| Speed prevents compounding damage | Extraction and drying within 24 to 48 hours prevents mold growth and limits repair costs that directly reduce resale value. |

| Documentation protects value | Appraisers require photos and repair records to minimize stigma deductions; undocumented repairs are treated as unresolved damage. |

| Repair often beats selling as-is | Completing structural and mold repairs typically recovers 10% to 20% in sale price, outperforming the deep discounts cash buyers demand. |

What I’ve learned after years of watching homeowners navigate this

The homeowners who come out of a water damage event with their equity intact share one trait: they acted fast and they documented everything. The ones who struggle are almost always the ones who waited, hoping the problem would dry out on its own, or who made repairs without keeping records.

What surprises most people is how much of the value loss comes from the financing side, not the physical damage itself. A home can look completely restored and still fail conventional underwriting if the appraisal report lacks documentation of remediation. I’ve seen sales fall apart not because the damage was severe, but because the seller couldn’t prove it had been properly addressed. That’s a painful and entirely avoidable outcome.

The mold timeline is the other thing I’d push every homeowner to take seriously. Twenty-four to forty-eight hours sounds like plenty of time, but in practice, most people spend the first day dealing with the shock of the event, contacting insurance, and trying to figure out who to call. By the time professional extraction starts, the clock has often already run out. Getting a restoration company on-site within hours, not days, is what separates a manageable repair from a gut renovation.

My honest advice: treat water damage as a financial emergency, not a home repair project. The decisions you make in the first 48 hours determine whether you’re looking at a $3,000 repair or a $40,000 one. And if you’re planning to sell within the next few years, every dollar you spend on proper remediation and documentation is worth two dollars in negotiating leverage when offers come in.

— Jim

Protect your home’s value with Zero Water Restoration

Water damage doesn’t give you time to research your options. Zero Water Restoration responds 24/7 throughout Schaumburg, Barrington, Arlington Heights, and the greater Chicagoland area, with a team trained to extract, dry, and document from the first hour on-site. Their water damage restoration services cover everything from emergency extraction to full reconstruction, and their mold remediation specialists produce the documented remediation reports that appraisers and lenders require. Zero Water Restoration also works directly with insurance adjusters to manage claims and keep your out-of-pocket costs as low as possible. Call (847) 515-7000 or visit zerowaterrestoration.com for a free inspection and estimate.

FAQ

Does water damage always lower home value?

Water damage lowers home value in nearly every case, with the severity depending on the type of damage, how quickly it was addressed, and whether professional remediation was documented. Fully repaired and documented damage causes less value loss than unresolved or undisclosed damage.

How much value does a home lose from water damage?

Homes with water damage history typically sell for 15% to 30% less than comparable undamaged properties. Severe untreated cases, particularly those sold as-is to investors, can fetch only 50% to 70% of the property’s after-repair value.

Can you get a mortgage on a water-damaged home?

Conventional lenders require that structural or safety-related water damage be repaired before loan delivery. Minor cosmetic damage may allow closing if repair funds are escrowed, but active leaks, mold, or compromised systems will stop mortgage approval under Fannie Mae and Freddie Mac guidelines.

How does repairing water damage affect resale value?

Completing repairs before listing typically recovers 10% to 20% in sale price compared to selling as-is. A stigma discount may still apply even after full remediation, but documented professional repairs reduce the appraiser’s deduction and restore access to conventional financing.

How fast does mold develop after water damage?

Mold begins colonizing within 24 to 48 hours of water intrusion. Professional extraction and drying within that window is the single most effective action for preventing mold growth and limiting the long-term impact on property value.