Most homeowners picture insurance companies and restoration contractors as a well-oiled machine working together to get life back to normal after water damage. The reality is messier. These two parties often have conflicting priorities, communicate on completely different timelines, and serve different masters. If you don’t understand how this relationship actually works, you risk getting less coverage than you’re entitled to, missing critical deadlines, or ending up with repairs that stop short of truly fixing your home. This guide pulls back the curtain on the full process so you can protect your interests from the moment damage happens to the day your home is fully restored.

Table of Contents

- Understanding the insurance and restoration partnership

- Step-by-step: How a restoration company coordinates with your insurer

- Common pitfalls: Gaps, denials, and who really advocates for you

- Maximizing your insurance claim with the right restoration partner

- The bottom line: What most homeowners get wrong about restoration and insurance

- Expert help for every step of your water damage insurance claim

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your roles | Restoration firms and insurers have different priorities, so understanding who does what puts you in control. |

| Document everything early | Careful records and photos from the start boost your chances in claim negotiations and appeals. |

| Beware of preferred vendors | Insurer-recommended restoration companies may put the insurer’s interests first, so vet your options. |

| Appeals are possible | If your claim is denied or underpaid, professional documentation can help you challenge the outcome. |

| Choose a local advocate | Selecting a knowledgeable, client-focused restoration partner helps maximize your insurance claim and peace of mind. |

Understanding the insurance and restoration partnership

Before anything else, get clear on who plays what role. An insurance adjuster works for your insurer. Their job is to evaluate your claim, assign a dollar value to the damage, and determine what your policy covers. They are not on your side, even when they seem helpful. A restoration contractor is hired to physically fix the damage. Depending on how you find them, they may or may not be motivated to advocate for the full scope of repairs you need.

Here’s where it gets complicated. Many major insurers run what are called preferred vendor programs. These are pre-screened lists of restoration companies that insurers recommend to policyholders after a claim. The catch? As noted in Water Damage Restoration Insurance Claims, preferred vendors can prioritize the insurer’s interests over the homeowner’s, meaning they may complete only what the insurer approves rather than what your home truly needs. They get volume business from the insurer in exchange for pricing agreements that keep claim costs down.

Understanding navigating water damage claims from the start helps you avoid these pitfalls before you’re already in the middle of them.

Key differences at a glance:

| Party | Hired by | Primary goal | Controls |

|---|---|---|---|

| Insurance adjuster | Your insurer | Minimize claim payout | Authorization of funds |

| Preferred vendor | Insurer (volume referral) | Complete job within insurer’s budget | Physical repairs |

| Independent restoration company | You | Restore home fully, document all damage | Physical repairs and documentation |

| Public adjuster | You | Maximize claim settlement | Claim negotiation |

What Illinois law requires of your insurer:

According to Water Damage Restoration Insurance Claims, Illinois timelines are specific. Your insurer must acknowledge your claim within 15 days, complete the investigation within 30 days, and issue a settlement or denial within 45 days. Missing these windows can be grounds for complaint with the Illinois Department of Insurance.

Pro Tip: Before your insurance adjuster ever sets foot in your home, take a full video walkthrough of the damage with timestamps. Open every cabinet, lift every rug, and capture water lines on walls. This documentation protects you if there’s any dispute later about the true extent of the damage. The adjuster’s notes are their record. Your video is yours.

When working with insurance providers, the right restoration partner knows how to speak the insurer’s language, submit properly formatted scopes of work, and push back when the adjuster undervalues something.

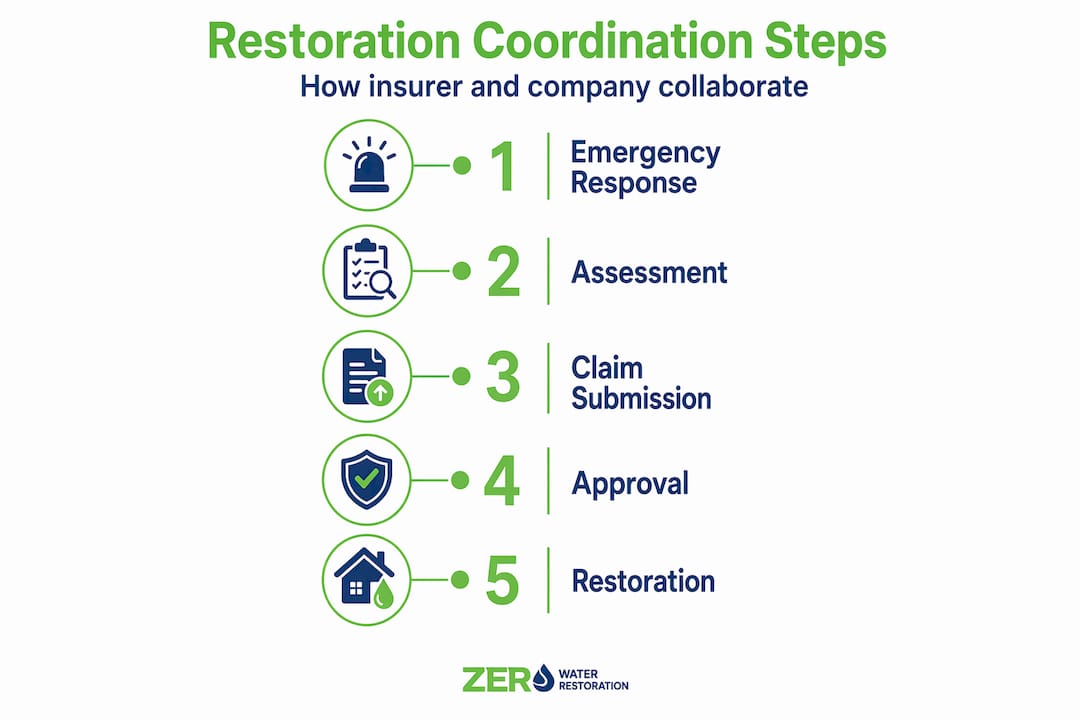

Step-by-step: How a restoration company coordinates with your insurer

Once damage is discovered, the clock starts ticking. Here’s exactly what happens when a reputable restoration company coordinates with your insurer:

-

Emergency response and stabilization. The restoration company arrives, stops active water intrusion, and begins extraction. This isn’t optional. Your policy almost certainly requires you to mitigate damage promptly, or the insurer can reduce your claim.

-

Damage documentation. The restoration team photographs and measures everything. Good companies use software like Xactimate, which generates line-item cost estimates using industry-standard pricing that adjusters recognize. This becomes your evidence file.

-

Claim initiation. You notify your insurer and file the claim. In Illinois, they have 15 days to acknowledge it. Your restoration company can help you frame the scope of the claim correctly from the beginning.

-

Adjuster inspection. The adjuster visits, takes their own measurements and photos, and creates their scope of loss. This is the insurer’s version of what happened and how much it costs to fix.

-

Scope comparison and negotiation. Here’s where conflicts emerge. The adjuster’s estimate and the restoration company’s estimate almost never match on the first pass. Line items get dropped, labor rates differ, and materials may be valued at depreciated costs instead of current replacement value.

-

Supplement negotiations. When restoration work reveals hidden damage, say, water behind walls or subfloor rot that wasn’t visible at first inspection, the restoration company submits a supplement to get additional funds approved. The average national restoration cost runs about $1,536 but can range from $721 to $3,526, and supplements for hidden damage are approved at lower rates than the initial claim, so strong documentation matters enormously.

-

Repair and completion. Once funds are authorized, physical restoration proceeds, including drying, demolition of damaged materials, and rebuilding. Certified restoration ensures this work meets industry standards.

-

Final documentation and close-out. The restoration company submits proof of completed work. You sign off. Your insurer releases the final payment.

Typical timeline for a water damage claim:

| Phase | Who’s responsible | Expected timeframe |

|---|---|---|

| Emergency mitigation | Restoration company | Within hours |

| Claim filing | Homeowner | Within 24 to 48 hours |

| Adjuster inspection | Insurer | Within 7 to 14 days |

| Scope negotiation | Restoration company and insurer | 5 to 21 days |

| Physical repairs | Restoration company | Varies by scope |

| Supplement approval | Insurer | Up to 30 additional days |

Pro Tip: If communication between your contractor and adjuster stalls, don’t wait. Call both parties yourself, document the call with a follow-up email, and set a date for a decision. You are the client. You have every right to drive the timeline.

For situations where you need to act before your insurer approves everything, knowing how to make temporary repairs can prevent the damage from getting worse and protect your claim.

Common pitfalls: Gaps, denials, and who really advocates for you

Even with the best preparation, claims can go sideways. Here are the most common breakdowns and what to do about them.

The preferred vendor loyalty problem. When your insurer sends a contractor, that contractor gets paid by the work they complete within the insurer’s agreed rates. They have little financial incentive to fight for additional line items or supplements. They want to finish the job quickly and move to the next referral. As noted by Insurance Repair Authority, insurers may undervalue damage through depreciation, use actual cash value instead of replacement cost, or omit line items entirely. Restoration firms that work for the homeowner push for full replacement cost value and negotiate aggressively on supplements.

Mold and delayed mitigation denials. This is one of the most frustrating traps. If you wait too long to address water damage, mold growth becomes what insurers call “consequential damage” rather than a direct result of the covered event. According to Water Damage Restoration Insurance Claims, mold claims from delayed mitigation may be denied outright. Act fast, and document every mitigation step with dates and photos.

Gradual damage vs. sudden damage. Policies typically cover sudden, accidental damage. A pipe that burst overnight is covered. A slow leak that eroded your subfloor over two years often isn’t. But gradual damage denials are appealable, especially when professional documentation shows the damage was not visible or detectable until it became acute.

What you can do:

- Get your own independent restoration company’s written estimate before agreeing to anything with the insurer’s preferred vendor

- Request every adjuster decision in writing with the specific policy language cited

- Keep a communication log with dates, names, and summaries of every call

- Ask your restoration company to attend the adjuster inspection as your representative

- Look into choosing the right restoration company before you need one

Know your Illinois rights. Your insurer must acknowledge your claim within 15 days of filing. They must complete their investigation within 30 days. They must issue a written settlement or denial within 45 days. If they miss these windows, file a complaint with the Illinois Department of Insurance at insurance.illinois.gov. You also have the right to hire your own restoration company regardless of your insurer’s recommendations.

When a public adjuster makes sense. For large or complex claims, a public adjuster works exclusively for you, negotiating with the insurer to maximize your settlement. They typically charge 10 to 15 percent of the claim total. For a $50,000 claim, that fee is significant. But if they recover $20,000 more than the insurer initially offered, the math works in your favor. Use them for major losses, not for minor water damage.

Maximizing your insurance claim with the right restoration partner

The most powerful thing you can do for your claim is choose your restoration partner wisely, before the adjuster sets the narrative.

-

Vet the company before hiring. Ask whether they use Xactimate or similar industry-standard estimating software. Ask if they have experience negotiating supplements. Confirm they carry proper licensing and insurance in Illinois. Check Google reviews and the Better Business Bureau, not just testimonials on their website.

-

Review the contract carefully. Avoid any contract that assigns your insurance benefits directly to the restoration company (an “assignment of benefits” agreement) without fully understanding what you’re signing. Make sure the contract specifies the full scope of work, not just emergency mitigation.

-

Exercise your right to choose. Illinois law does not require you to use your insurer’s preferred vendor. As explicitly noted in Water Damage Restoration Insurance Claims, preferred vendors can prioritize the insurer’s interests over yours. You have the legal right to select your own contractor.

-

Build your documentation file. Save every receipt, from hotel costs during displacement to materials for temporary repairs. Photograph every phase of restoration work. Request a copy of your restoration company’s job file including moisture readings, drying logs, and material removal records. All of this supports your claim, and it all strengthens an appeal if the insurer underpays.

-

Use the claim navigation guide as your roadmap. Having a documented process to follow reduces errors and keeps your claim on track even when things get stressful.

Pro Tip: Never rely solely on your insurer’s preferred vendor when the damage involves mold, structural materials, or anything that isn’t immediately visible. These are exactly the situations where a vendor with loyalty to the insurer’s budget will underperform. Your home is worth more than a fast close-out.

The bottom line: What most homeowners get wrong about restoration and insurance

After a decade of working through water damage claims alongside homeowners across the northwest suburbs of Chicago, we’ve seen the same mistake repeated more than any other. Homeowners trust the process too much at the beginning, and fight back too late.

When someone calls their insurer, files the claim, lets the adjuster come out, and accepts the first number offered, they often leave thousands of dollars on the table without knowing it. They assume the system is designed to make them whole. In reality, the system is designed to manage costs. That’s not a criticism. It’s simply how insurance works.

The homeowners who come out whole are the ones who show up documented, informed, and partnered with a restoration company that knows how to advocate for them. They ask why line items were removed. They push for replacement cost value instead of depreciated actual cash value. They get supplements approved for hidden damage because their contractor was thorough enough to find it and document it.

What most restoration guides never mention is the emotional weight of this process. You’re dealing with a damaged home, possible displacement, and mountains of paperwork, all at the same time. The right restoration partner doesn’t just fix the physical damage. They carry the insurance process with you, so you’re not doing it alone at midnight trying to understand what your policy actually says about subfloor coverage.

Building real trust in restoration isn’t a marketing phrase. It’s the difference between a homeowner who recovers fully and one who settles for less because the process wore them down.

Expert help for every step of your water damage insurance claim

Dealing with water damage is stressful enough without also trying to decode adjuster estimates and policy exclusions on your own. That’s exactly where having a knowledgeable restoration team in your corner makes an enormous difference.

Zero Water Restoration has spent over 10 years guiding homeowners through water damage claims in Barrington, Lake Zurich, Palatine, and communities across the northwest suburbs. From the moment we arrive on scene, we document everything, communicate directly with your adjuster, and fight for the full value of your claim. Whether you’re dealing with a burst pipe, storm flooding, or mold remediation after untreated moisture, our team handles it start to finish. If you need Barrington water damage help or anywhere nearby, call us 24/7 at (847) 515-7000 or visit zerowaterrestoration.com for a free inspection.

Frequently asked questions

What if the insurance company’s preferred restoration vendor is not my first choice?

You can select your own restoration company in virtually all cases. As confirmed by Water Damage Restoration Insurance Claims, preferred vendors prioritize the insurer’s interests, and your insurer cannot legally require you to use one.

How long does an insurer have to process my water damage claim in Illinois?

Illinois law requires insurers to acknowledge your claim within 15 days, complete the investigation within 30 days, and issue a settlement or denial within 45 days, as specified by Illinois claim timelines.

Will my insurance cover mold caused by water damage?

Coverage depends heavily on timing. Mold from delayed mitigation is often denied as consequential damage, so act immediately, document your mitigation steps, and keep all records dated.

How much does water damage restoration typically cost?

Nationally, the average restoration cost is about $1,536, with a range from $721 to $3,526 before your deductible, and complex or hidden damage can push costs significantly higher.

Can I appeal if my insurance claim is denied or underpaid?

Yes, and you should. Denials for gradual damage and underpaid claims are both appealable, especially when a professional restoration company provides detailed documentation to support the full scope of damage.