Homeowners insurance covers mold remediation only when mold results from a covered peril, such as a burst pipe or fire suppression water. The industry term for this is “covered peril causation,” and it is the single factor that determines whether your insurer pays or denies your claim. Most homeowners assume their policy covers mold as a standalone problem. It does not. Coverage depends entirely on what caused the moisture that allowed mold to grow. Understanding this distinction is the first step toward filing a successful mold damage insurance claim.

Why mold remediation is covered by insurance: the core rule

Mold coverage is tied to the cause of the water event, not to the mold itself. This is the most common misconception homeowners carry into a claim. Insurers do not cover mold as a separate line item. They cover mold as a consequence of covered water damage, and only when that water damage was sudden and accidental.

The standard HO-3 homeowners policy is the most widely held policy type in the United States. Under HO-3 terms, causation is the deciding factor: if the moisture event that produced mold growth qualifies as a named covered peril, remediation costs fall within the policy’s scope. If the moisture came from neglect, long-term humidity, or a slow leak you ignored, the claim will be denied.

This framework exists because insurers design policies to cover unexpected losses, not maintenance failures. A burst pipe at 2 AM is unexpected. A slow drip under your sink that you noticed six months ago is not. That distinction drives every mold remediation insurance coverage decision your adjuster makes.

What water damage events qualify as covered perils?

Certain water damage events consistently qualify as covered perils under standard homeowners policies. Knowing which ones apply protects you before a problem starts.

Covered events that typically qualify:

- Burst or frozen pipes

- Accidental appliance overflow (washing machine, dishwasher, water heater)

- Fire suppression water from sprinkler systems

- Storm damage that causes a sudden roof breach and interior water intrusion

- Accidental discharge from plumbing systems

Events that are typically excluded:

- Flooding from external water sources (rivers, storm surge, heavy rain runoff)

- Sewer backup without a specific endorsement

- Slow seepage through foundation walls

- Condensation buildup from poor ventilation

- Mold from long-term humidity in a basement or crawl space

Homeowners insurance pays for mold remediation resulting from sudden water damage events, including emergencies like burst pipes or fire suppression water. Mold from maintenance-related or long-term moisture accumulation is not covered. The word “sudden” is doing a lot of work in that sentence. It means the event happened without warning and was not the result of deferred maintenance.

Storm damage deserves a closer look. If a storm tears off shingles and rain enters your attic, that qualifies as sudden water intrusion. If your roof was already deteriorating and rain eventually worked its way through, the claim becomes harder to support. For roof-related water events, understanding how to file a storm damage claim correctly from the start protects your position with the adjuster.

Pro Tip: Document every water event in your home immediately, even minor ones. A photo with a timestamp creates a record that supports the “sudden” classification if mold appears weeks later.

How do policy limits and endorsements affect your payout?

Knowing you have coverage is only half the answer. Knowing how much coverage you actually have is the other half.

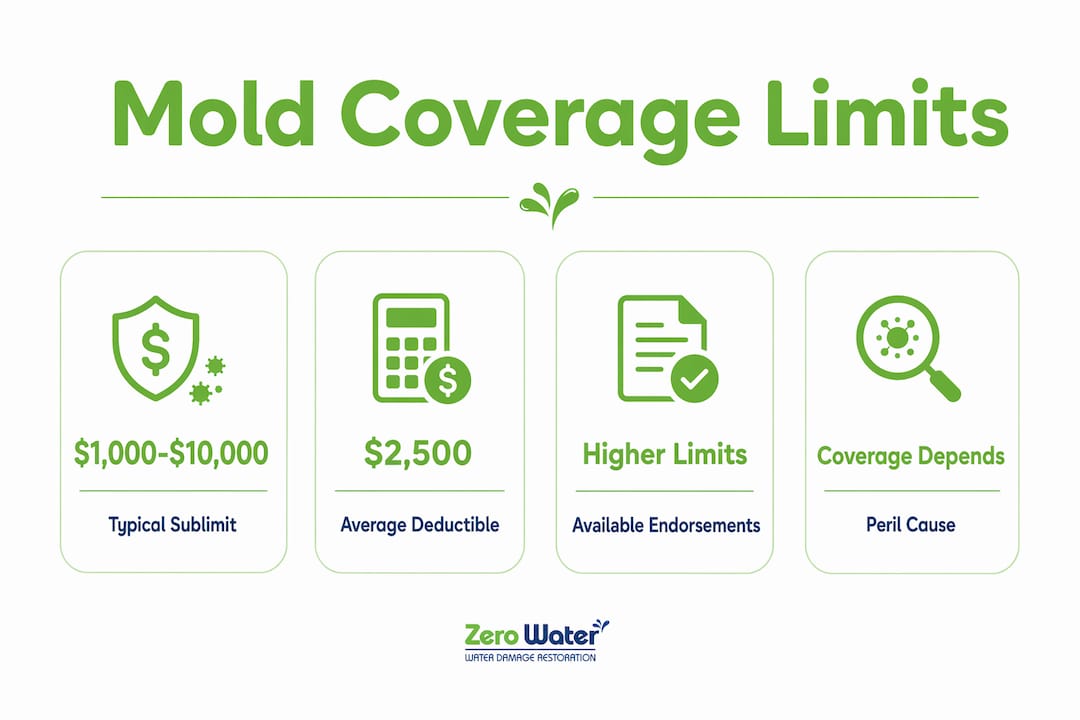

Many HO-3 policies cap mold remediation at a sublimit of $1,000 to $10,000. That range sounds reasonable until you get a remediation quote for a finished basement or a wall cavity with significant growth. Professional mold remediation in the Chicagoland area routinely exceeds those sublimits, which means you could have a valid claim and still owe thousands out of pocket.

Your policy deductible applies to the underlying covered event, not to the mold separately. If your deductible is $2,500 and your mold sublimit is $5,000, your maximum net payout from the insurer is $2,500. That math surprises a lot of homeowners at the worst possible moment.

| Scenario | Base coverage | Mold sublimit | Endorsement added | Effective mold coverage |

|---|---|---|---|---|

| No endorsement, low sublimit | HO-3 standard | $1,000 | None | $1,000 max |

| No endorsement, mid sublimit | HO-3 standard | $5,000 | None | $5,000 max |

| Mold endorsement added | HO-3 standard | $5,000 | Yes | $10,000–$25,000+ |

| Mold buy-back rider | HO-3 enhanced | $10,000 | Full buy-back | Broader coverage |

Mold remediation costs frequently exceed typical HO-3 policy sublimits, so experts advise obtaining mold-specific endorsements or buy-backs for better protection. An endorsement is an add-on to your existing policy that raises the mold sublimit or removes it entirely. The annual premium increase for a mold endorsement is usually modest compared to what remediation actually costs.

Pro Tip: Call your insurance agent today and ask specifically what your mold sublimit is. Most homeowners have never checked, and the answer is almost always lower than they expect.

Why do insurers separate “sudden” from “gradual” moisture damage?

The sudden versus gradual distinction is not arbitrary. It reflects how insurers evaluate risk and determine whether a loss was preventable.

Insurers often use a 14-day boundary to define gradual water damage. If moisture was seeping into your home for more than 14 days before you reported it, the insurer may classify the event as gradual, regardless of when mold became visible. That classification alone can end your claim.

Here is how insurers reconstruct the timeline when you file a mold claim:

- Review the date of the triggering event. When did the pipe burst, the appliance fail, or the storm occur? This date anchors the timeline.

- Examine when you reported the damage. A gap of days is acceptable. A gap of weeks raises questions.

- Assess physical evidence. Adjusters look at how far mold has spread, how dry or wet materials are, and whether staining suggests long-term exposure.

- Request documentation. Photos, plumber invoices, service logs, and even text messages to a landlord or contractor all factor into the classification.

- Classify the event. The adjuster labels the cause as sudden or gradual, and that label determines coverage eligibility.

Claims success often depends on causation evidence and moisture timeline reconstruction rather than mold presence alone. You can have visible mold everywhere and still lose a claim if the timeline suggests you knew about the moisture and did nothing.

Quick detection and fast reporting are your two strongest tools. The moment you find water damage, document it with photos and contact your insurer. Do not wait to see if it dries out on its own.

Pro Tip: Keep a simple home maintenance log. Note the date any plumber, roofer, or contractor visits your property. That log becomes evidence of responsible ownership if a mold claim is ever disputed.

How does mold coverage differ when flooding is the cause?

Flooding is the most common source of confusion in mold remediation insurance coverage, and the rule here is straightforward: standard homeowners insurance does not cover mold caused by flooding.

Standard homeowners insurance excludes flood-related mold damage entirely. Flooding is defined as water that enters a home from an external source, such as a river overflow, storm surge, or heavy rain runoff that pools on the ground. That definition is distinct from a burst pipe or appliance failure, which are internal water events.

Flood insurance through the National Flood Insurance Program (NFIP) does exist, but its mold coverage is limited. NFIP flood policies cover mold only under specific conditions, typically when flooding made the home inaccessible and remediation was delayed as a result. That is a narrow window.

What to know about mold coverage and excluded water sources:

- Sewer backup and sump pump failure are excluded from standard policies but can be added through a water and sewage backup endorsement.

- Mold from backed-up drains or broken sump pumps may be covered under these endorsements, but ongoing seepage issues remain excluded.

- Homeowners in flood-prone areas, including parts of the greater Chicagoland region, should carry both NFIP flood insurance and a sewer backup endorsement.

- Reviewing your policy before a flood season is more effective than reviewing it after a loss.

For homeowners who have already experienced flooding, understanding how restoration prevents mold after a flood event is the practical next step, regardless of what your policy covers.

Key Takeaways

Mold remediation is covered by insurance only when mold results from a sudden, accidental covered peril, and coverage amounts are almost always limited by sublimits that homeowners should verify and supplement with endorsements.

| Point | Details |

|---|---|

| Causation drives coverage | Insurance pays for mold only when a covered peril, like a burst pipe, caused the moisture. |

| Sublimits cap your payout | Most HO-3 policies limit mold coverage to $1,000–$10,000; endorsements raise that ceiling. |

| Sudden vs. gradual is decisive | Insurers use a 14-day benchmark to classify moisture events; late reporting can end a claim. |

| Flooding requires separate coverage | Standard policies exclude flood-related mold; NFIP flood insurance has its own narrow mold conditions. |

| Documentation wins claims | Photos, service logs, and fast reporting are the strongest tools for a successful mold claim. |

What I have learned after years of mold claims

The homeowners who struggle most with mold claims are not the ones with the worst damage. They are the ones who waited.

I have seen situations where a slow drip under a bathroom vanity went unaddressed for weeks because the homeowner assumed it would resolve itself or was not serious enough to call about. By the time mold appeared on the drywall, the moisture timeline was already working against them. The insurer classified it as gradual damage, and the claim was denied. The remediation cost came entirely out of pocket.

The other pattern I see constantly is homeowners who assume their policy covers “mold” as a category. It does not. Coverage is for mold as a result of covered water damage, and that result is subject to sublimits that most people have never read. I have talked to homeowners who assumed they had full coverage, filed a claim, and then discovered their mold sublimit was $2,000 on a $15,000 remediation job.

My honest advice: read your declarations page today. Find the mold sublimit. If it is under $10,000, call your agent and ask about a mold endorsement. The premium difference is usually small. The financial difference when you need it is enormous.

Working with a restoration company that understands the insurance process also changes outcomes. When documentation is gathered correctly, when the timeline is established clearly, and when the adjuster has everything they need from day one, claims move faster and pay better. That is not luck. That is preparation.

— Jim

Mold remediation help when you need it most

Discovering mold in your home is stressful. Figuring out what your insurance covers on top of that makes it worse.

Zerowaterrestoration has worked with homeowners across Schaumburg, Barrington, Arlington Heights, and the broader Chicagoland area for over 10 years. The team handles professional mold remediation from inspection through full restoration, and works directly with insurance adjusters to document damage, establish timelines, and support your claim from the start. If you have experienced water damage or discovered mold growth, call (847) 515-7000 for a free inspection. The sooner you act, the stronger your claim position. You can also review the water damage restoration process to understand what happens after you make the call.

FAQ

Does homeowners insurance cover mold removal?

Homeowners insurance covers mold removal only when mold results from a covered peril, such as a burst pipe or accidental appliance overflow. Mold from flooding, neglect, or slow leaks is generally excluded.

What is the typical mold sublimit on a homeowners policy?

Most HO-3 policies cap mold remediation coverage at $1,000 to $10,000. Homeowners can raise that limit by adding a mold-specific endorsement or buy-back rider to their policy.

Why do insurers deny mold claims from gradual leaks?

Insurers exclude gradual moisture damage because it reflects a maintenance failure rather than an unexpected loss. A 14-day benchmark is commonly used to distinguish sudden events from ongoing seepage.

Does flood insurance cover mold?

NFIP flood insurance covers mold only under narrow conditions, typically when flooding made the home inaccessible and delayed remediation. Standard homeowners policies exclude flood-related mold entirely.

How can I strengthen a mold remediation insurance claim?

Document the triggering water event immediately with photos and timestamps, report it to your insurer without delay, and keep records of any contractor or plumber visits. Causation evidence and a clear timeline are the two factors that most influence claim approval.